Stablecoin yield strategies for the 2026 bear market

Stablecoin yield strategies for the 2026 bear market

Stablecoin yield strategies for the 2026 bear market

Stablecoin yield strategies for the 2026 bear market

Bitcoin is sitting around $64,000, down roughly 49% from its $126,000 all-time high last October. The Crypto Fear and Greed Index hit a record low of 5 earlier this month before recovering to 16. Most portfolios are deep in the red. And yet, the stablecoin market just crossed $310 billion, a new all-time high. That gap tells you something: money is not leaving crypto. It is moving to safety.

Pistachio.fi is a self-custody DeFi yield platform that helps you earn on stablecoins without giving up control of your funds. It offers curated vaults across vetted protocols, risk grades for every option, and zero gas fees. This article breaks down where stablecoin yields actually come from in 2026, which strategies make sense during a bear market, and how new regulations like the GENIUS Act affect your options.

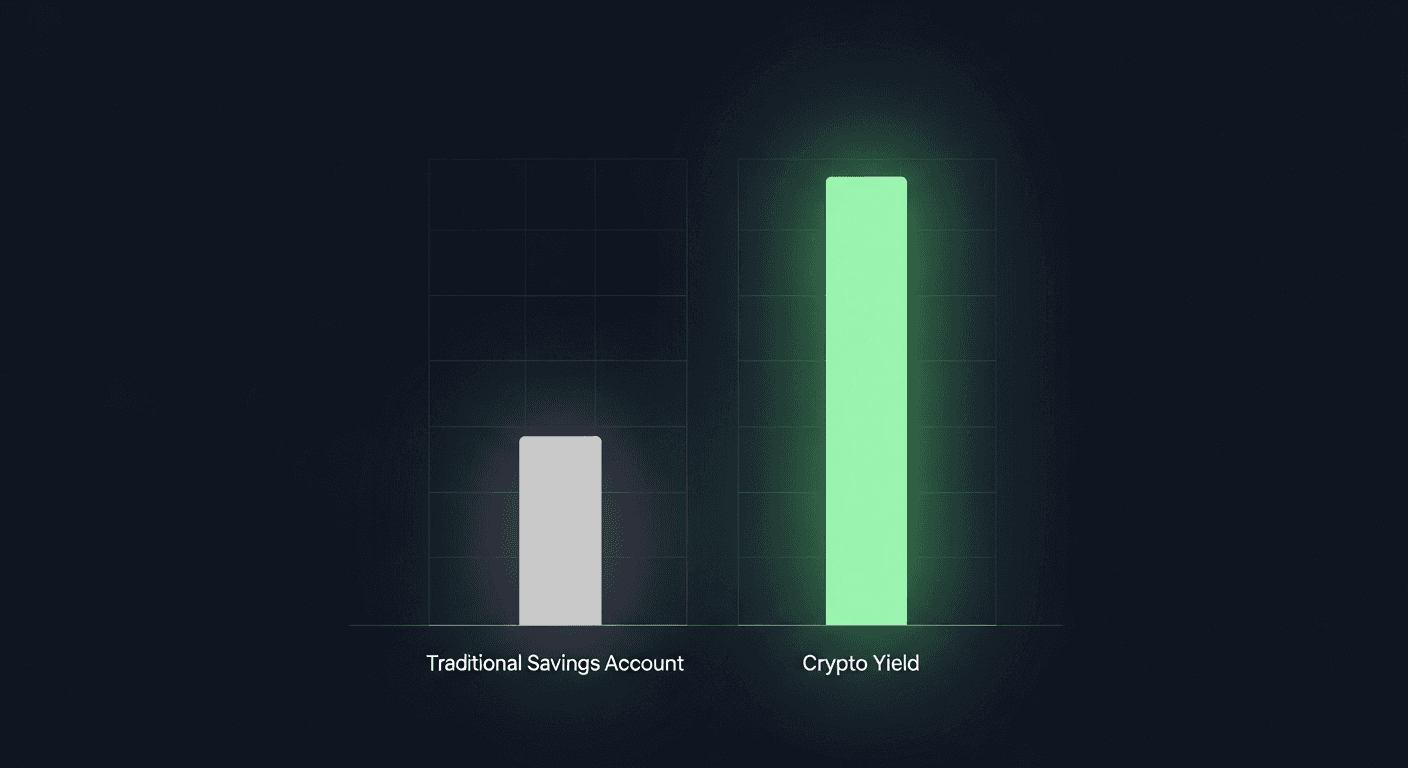

TL;DR: In the current bear market, stablecoin holders can earn 3% to 8% APY through DeFi lending protocols like Aave and Morpho, with higher rates available through fixed-yield instruments like Pendle or yield-bearing stablecoins like sUSDe. The GENIUS Act bans custodial issuers from paying yield on stablecoins, but DeFi protocols and self-custody wallets are explicitly exempt. Platforms like Pistachio.fi aggregate these DeFi yields into curated vaults with risk grades, though alternatives like DefiLlama's yield dashboard also let users compare rates across protocols manually.

What you need to know

DeFi stablecoin lending yields range from 3% to 8% APY on major protocols, with variable rates tied to borrowing demand.

The GENIUS Act's yield ban applies only to custodial stablecoin issuers. DeFi lending, liquidity provision, and self-custody wallets remain fully legal.

Bear markets compress yields but also reduce smart contract risk, since fewer speculators means less protocol strain.

A core-satellite approach (most funds in conservative lending, a smaller allocation in higher-yield strategies) works best during drawdowns.

Self-custody matters more than ever. Platforms that hold your keys can freeze withdrawals when markets panic.

Why are stablecoin yields still available during a bear market?

Stablecoin yields do not come from token price appreciation. They come from people borrowing. Even in a bear market, traders borrow stablecoins to short assets, hedge positions, or fund arbitrage. As long as someone wants to borrow your USDC, you earn interest.

That said, bear markets typically compress yields. When fewer traders are borrowing on margin, demand drops, and so does the rate lenders earn. According to DefiLlama, stablecoin lending rates on major protocols have settled into a 3% to 8% range during the current downturn, compared to the 8% to 15% rates common during the bull run peaks of mid-2025.

This is actually good news for conservative depositors. Lower yields usually correlate with lower protocol risk. There is less borrowed capital sloshing around the system, less chance of cascading liquidations, and less pressure on smart contracts. The DeFi ecosystem's total value locked sits near $130 billion (per DefiLlama), and Aave alone holds $27 billion, having just crossed $1 trillion in cumulative lending volume. These are not fragile, experimental systems anymore.

What are the main strategies for earning yield on stablecoins right now?

There are five primary ways to earn yield on stablecoins in 2026. Each comes with a different risk and return profile. Here is how they compare.

Strategy | Typical APY range | Risk level | Complexity | Best for |

|---|---|---|---|---|

DeFi lending (Aave, Compound, Morpho) | 3% to 7% | Low to moderate | Low | Core allocation, passive income |

Yield-bearing stablecoins (sUSDe, sDAI/sUSDS) | 4% to 8% | Moderate | Low | Hands-off holders who want auto-compounding |

Fixed-rate vaults (Pendle) | 5% to 10% | Moderate | Medium | Locking in rates when you expect further compression |

Stablecoin liquidity provision (Curve, Uniswap) | 2% to 6% | Moderate | Medium | Earning swap fees on high-volume pairs |

Tokenized treasuries (onchain T-bills) | 4% to 5% | Low | Low | Lowest-risk option, tied to U.S. government rates |

DeFi lending: the workhorse

Depositing stablecoins into lending protocols like Aave, Compound, or Morpho is the most straightforward strategy. You supply USDC or USDT, borrowers pay interest, and you collect a variable rate. Aave currently holds around $20 billion in stablecoin deposits and commands over 80% of Ethereum's stablecoin lending market.

The rates fluctuate. During a liquidation cascade (like the one on February 5 when Bitcoin dropped 6 standard deviations in a single day), borrowing demand spikes and your APY temporarily jumps. During quiet weeks, rates drift lower. Over a full cycle, 4% to 6% is a reasonable expectation for major protocols.

Morpho deserves special mention. It operates as an optimization layer that creates isolated lending markets with customizable risk parameters. With over $8.5 billion in peak deposits and 25+ security audits, it has become the preferred venue for more sophisticated depositors who want to fine-tune their risk exposure. Understanding these DeFi risks is worth your time before committing capital.

Yield-bearing stablecoins

Instead of depositing into a lending pool yourself, you can hold a stablecoin that generates yield automatically. Ethena's sUSDe earns from perpetual futures funding rates and staked ETH yield. Sky's sUSDS (formerly sDAI) earns from Sky protocol's lending and real-world asset revenue.

The advantage is simplicity. You hold the token and yield accrues. The risk is that these tokens carry the smart contract risk of the underlying protocol, plus the specific mechanism risk of however that yield is generated. sUSDe, for example, depends on funding rates remaining positive on average. In a prolonged bear market, funding can flip negative for extended periods.

Fixed-rate strategies with Pendle

Pendle lets you split yield-bearing assets into principal and yield components. If you expect rates to fall further, you can lock in today's rate by buying the principal token at a discount. Pendle recently launched a stUSDS pool with Spark Protocol offering around 16.8% APY, though that elevated rate reflects short-term incentives and high borrowing demand rather than sustainable income.

Fixed-rate strategies add complexity. You are dealing with maturity dates (for example, the stUSDS pool matures June 25, 2026), potential liquidity issues if you need to exit early, and the learning curve of understanding yield tokenization. But for someone who wants predictability, locking in 5% to 7% for six months can be more appealing than watching variable rates bounce around.

Stablecoin liquidity provision

Providing liquidity to stablecoin trading pairs (USDC/USDT on Curve, for instance) earns you a share of swap fees. Because stablecoins trade close to $1, impermanent loss is minimal in normal conditions. The risk is a depeg event. If one stablecoin in the pair loses its peg, your position takes a real hit.

In a bear market, trading volumes tend to drop, which means lower fees. This makes LPing less attractive than lending for most people. It still has a role if you are comfortable with the specific pairs and want diversified yield sources.

Tokenized treasuries

The lowest-risk option in DeFi right now is onchain tokenized U.S. Treasury bills. Products from protocols like Ondo, Backed, and Maple give you exposure to short-term government debt with yields around 4% to 5%. The yield comes from the U.S. government, not from crypto markets. The main risks are smart contract risk on the wrapper and potential regulatory changes to the tokenized securities space.

How does the GENIUS Act affect stablecoin yield?

The GENIUS Act, signed into law in 2025, established the first federal regulatory framework for payment stablecoins in the United States. On February 26, 2026, the OCC published a 376-page proposed rulemaking to implement the Act. One of the most talked-about provisions is the yield ban.

Here is what the ban actually says: authorized payment stablecoin issuers (think Circle, Tether, or any bank issuing a regulated stablecoin) are prohibited from distributing yield, interest, or rewards tied to stablecoin ownership. The OCC's draft goes further, creating a "regulatory presumption" that even indirect or affiliate-based reward structures could violate the Act.

But the exemptions matter more than the ban for most DeFi users.

DeFi and self-custody are exempt

The GENIUS Act explicitly excludes distributed ledger protocols (DeFi), development activities, immutable and self-custodial wallet interfaces, and liquidity pool participation from the definition of "digital asset service provider." In plain language: if you are lending USDC on Aave through a self-custody wallet, the yield ban does not apply to you.

This distinction is why the current White House negotiations on stablecoin yield are so important. The administration has held at least three meetings in February 2026 between crypto companies and banks, with the latest on February 19 reportedly making "progress." According to CoinDesk, the White House favors allowing limited stablecoin rewards while banks push back, arguing that yield-bearing stablecoins could compete with their deposit business.

The practical upshot: the yield ban pushes more activity toward DeFi. If Circle cannot pay you yield on USDC directly, your best option is to deposit that USDC into a lending protocol yourself. Self-custody platforms like Pistachio.fi, which use MPC wallets through PortalHQ to keep you in control of your keys, are positioned well for this exact scenario.

Building a bear market stablecoin portfolio

The goal during a bear market is not maximizing yield. It is preserving capital, staying liquid, and earning a real return above inflation while you wait for better conditions. Here is a practical allocation framework.

The core-satellite approach

The core portion (60–70% of holdings) goes into established lending protocols like Aave and Compound, or tokenized treasuries. Accept 3–5% APY in exchange for high liquidity and battle-tested smart contracts. This is your safety net.

The satellite allocation (20–30%) targets higher-yield strategies: Morpho vaults with optimized risk parameters, fixed-rate positions on Pendle, or yield-bearing stablecoins. Target 5–8% APY with slightly higher risk.

Reserve 10–20% as plain stablecoins with no yield exposure. When opportunities appear (a protocol launches new incentives, a temporary dislocation creates elevated rates), you want capital ready to deploy.

Risk management rules that actually matter

Diversify across protocols, not just strategies. If you put everything into Aave, you carry Aave's smart contract risk on 100% of your portfolio.

Check the audit history of any protocol you deposit into. Morpho has 25+ audits. Some newer protocols have one or none.

Watch utilization rates. When a lending pool's utilization climbs above 90%, withdrawal liquidity dries up. You might not be able to exit when you need to.

Avoid chasing double-digit APYs on new protocols. High yields in a bear market almost always come from token emissions that will end, or from mechanisms you do not fully understand. The protocols offering 20%+ on stablecoins right now are either running temporary incentive programs or taking on risk you should know about.

Pistachio.fi addresses several of these concerns structurally. Its curated investment vaults are selected by experts who evaluate protocol risk. Every option carries a risk grade so you can compare before you commit. The platform is completely gasless (zero transaction fees), which means the yield you see is closer to the yield you actually keep. And since Pistachio uses self-custody through MPC wallets, your funds never sit in a custodial hot wallet that could be frozen or hacked.

How does self-custody change the equation?

The 2022 bear market taught a painful lesson. Celsius, Voyager, BlockFi, and FTX all froze withdrawals when conditions deteriorated. Users who had deposited stablecoins for yield found their funds locked in bankruptcy proceedings. Some are still waiting for partial recovery four years later.

Self-custody removes this risk entirely. When you hold your keys (or use an MPC wallet where you control the key shares), no company can prevent you from withdrawing. Your stablecoins sit in smart contracts, not on a company's balance sheet.

This is not just a philosophical preference. It is a regulatory trend. The GENIUS Act's DeFi exemptions effectively reward self-custody users with continued access to yield. The OCC's framework treats custodial stablecoins like stored-value products (no yield allowed), while self-directed DeFi activity remains outside the ban's scope.

Pistachio.fi's approach uses PortalHQ's MPC wallet technology, which splits your private key into shares so that no single party (including Pistachio) can access your funds unilaterally. Combined with its neobank-like interface, it bridges the gap between the security of self-custody and the convenience of a managed platform.

Tax implications of stablecoin yield

Stablecoin yield is taxable income in most jurisdictions, including the United States. The IRS treats DeFi lending interest as ordinary income, taxed at your marginal rate in the year you receive it. This applies whether you claim the yield manually or it auto-compounds.

Tracking this across multiple protocols, chains, and strategies can be a headache. Every deposit, withdrawal, claim, and swap is a taxable event that needs documentation. Pistachio.fi integrates with Awaken.Tax for one-click tax export, which saves hours of spreadsheet work at the end of the year. If you are using multiple protocols manually, make sure you have a tracking solution in place before you start.

Frequently asked questions

What APY can I expect on stablecoins during a bear market?

Most DeFi lending protocols offer 3% to 7% APY on stablecoins during the current bear market. Rates vary based on borrowing demand, with temporary spikes during volatility events. Fixed-rate options through Pendle can lock in 5% to 10%, and yield-bearing stablecoins like sUSDe or sUSDS target 4% to 8%.

Is stablecoin yield still legal under the GENIUS Act?

Yes, for DeFi users. The GENIUS Act's yield ban applies only to custodial payment stablecoin issuers (like Circle or banks). DeFi protocols, self-custody wallets, and liquidity pool participation are explicitly exempt from the ban. The OCC confirmed this in its February 26, 2026 proposed rulemaking.

What is the safest way to earn yield on stablecoins?

The safest approach is lending USDC or USDT on established protocols like Aave or Compound, which have billions in deposits and years of operating history. Tokenized U.S. Treasury products offer even lower risk at 4% to 5% APY, since the yield comes from government bonds rather than crypto borrowing markets. Always use a self-custody wallet to avoid counterparty risk.

Can I lose money on stablecoins?

Yes. Stablecoins can depeg from $1, and the smart contracts holding your deposits can be exploited. Protocol insolvency (as seen with Terra/UST in 2022) can cause total loss. Even well-audited protocols carry residual smart contract risk. Diversifying across protocols and sticking to the most battle-tested options reduces but does not eliminate this risk.

How does Pistachio.fi compare to using DeFi protocols directly?

Pistachio.fi aggregates DeFi yields from vetted protocols into curated vaults, adds expert risk grades, and eliminates gas fees. You maintain self-custody through MPC wallets. The tradeoff compared to direct protocol access is that you rely on Pistachio's curation rather than choosing protocols yourself, and you use their interface rather than interacting with smart contracts directly. For most users, the convenience, risk filtering, and zero gas fees outweigh the reduced control.

Should I move all my crypto to stablecoins during a bear market?

That depends on your conviction and time horizon. Going 100% stablecoins means you avoid further drawdowns, but you also miss the recovery. A common approach is to hold a larger stablecoin allocation than you would during a bull market (say 40% to 60% of your portfolio) and earn yield while you wait. Dollar-cost averaging back into BTC or ETH at lower prices is another option that stablecoin yield can fund.

What happens to stablecoin yields if Bitcoin keeps dropping?

Further price drops typically reduce borrowing demand, which compresses lending yields. However, sharp selloffs can temporarily spike rates as traders scramble to borrow stablecoins for margin calls and liquidations. Over a sustained bear market, expect yields to settle toward the lower end of the 3% to 7% range, but they rarely go to zero because some borrowing demand always exists.

Bitcoin is sitting around $64,000, down roughly 49% from its $126,000 all-time high last October. The Crypto Fear and Greed Index hit a record low of 5 earlier this month before recovering to 16. Most portfolios are deep in the red. And yet, the stablecoin market just crossed $310 billion, a new all-time high. That gap tells you something: money is not leaving crypto. It is moving to safety.

Pistachio.fi is a self-custody DeFi yield platform that helps you earn on stablecoins without giving up control of your funds. It offers curated vaults across vetted protocols, risk grades for every option, and zero gas fees. This article breaks down where stablecoin yields actually come from in 2026, which strategies make sense during a bear market, and how new regulations like the GENIUS Act affect your options.

TL;DR: In the current bear market, stablecoin holders can earn 3% to 8% APY through DeFi lending protocols like Aave and Morpho, with higher rates available through fixed-yield instruments like Pendle or yield-bearing stablecoins like sUSDe. The GENIUS Act bans custodial issuers from paying yield on stablecoins, but DeFi protocols and self-custody wallets are explicitly exempt. Platforms like Pistachio.fi aggregate these DeFi yields into curated vaults with risk grades, though alternatives like DefiLlama's yield dashboard also let users compare rates across protocols manually.

What you need to know

DeFi stablecoin lending yields range from 3% to 8% APY on major protocols, with variable rates tied to borrowing demand.

The GENIUS Act's yield ban applies only to custodial stablecoin issuers. DeFi lending, liquidity provision, and self-custody wallets remain fully legal.

Bear markets compress yields but also reduce smart contract risk, since fewer speculators means less protocol strain.

A core-satellite approach (most funds in conservative lending, a smaller allocation in higher-yield strategies) works best during drawdowns.

Self-custody matters more than ever. Platforms that hold your keys can freeze withdrawals when markets panic.

Why are stablecoin yields still available during a bear market?

Stablecoin yields do not come from token price appreciation. They come from people borrowing. Even in a bear market, traders borrow stablecoins to short assets, hedge positions, or fund arbitrage. As long as someone wants to borrow your USDC, you earn interest.

That said, bear markets typically compress yields. When fewer traders are borrowing on margin, demand drops, and so does the rate lenders earn. According to DefiLlama, stablecoin lending rates on major protocols have settled into a 3% to 8% range during the current downturn, compared to the 8% to 15% rates common during the bull run peaks of mid-2025.

This is actually good news for conservative depositors. Lower yields usually correlate with lower protocol risk. There is less borrowed capital sloshing around the system, less chance of cascading liquidations, and less pressure on smart contracts. The DeFi ecosystem's total value locked sits near $130 billion (per DefiLlama), and Aave alone holds $27 billion, having just crossed $1 trillion in cumulative lending volume. These are not fragile, experimental systems anymore.

What are the main strategies for earning yield on stablecoins right now?

There are five primary ways to earn yield on stablecoins in 2026. Each comes with a different risk and return profile. Here is how they compare.

Strategy | Typical APY range | Risk level | Complexity | Best for |

|---|---|---|---|---|

DeFi lending (Aave, Compound, Morpho) | 3% to 7% | Low to moderate | Low | Core allocation, passive income |

Yield-bearing stablecoins (sUSDe, sDAI/sUSDS) | 4% to 8% | Moderate | Low | Hands-off holders who want auto-compounding |

Fixed-rate vaults (Pendle) | 5% to 10% | Moderate | Medium | Locking in rates when you expect further compression |

Stablecoin liquidity provision (Curve, Uniswap) | 2% to 6% | Moderate | Medium | Earning swap fees on high-volume pairs |

Tokenized treasuries (onchain T-bills) | 4% to 5% | Low | Low | Lowest-risk option, tied to U.S. government rates |

DeFi lending: the workhorse

Depositing stablecoins into lending protocols like Aave, Compound, or Morpho is the most straightforward strategy. You supply USDC or USDT, borrowers pay interest, and you collect a variable rate. Aave currently holds around $20 billion in stablecoin deposits and commands over 80% of Ethereum's stablecoin lending market.

The rates fluctuate. During a liquidation cascade (like the one on February 5 when Bitcoin dropped 6 standard deviations in a single day), borrowing demand spikes and your APY temporarily jumps. During quiet weeks, rates drift lower. Over a full cycle, 4% to 6% is a reasonable expectation for major protocols.

Morpho deserves special mention. It operates as an optimization layer that creates isolated lending markets with customizable risk parameters. With over $8.5 billion in peak deposits and 25+ security audits, it has become the preferred venue for more sophisticated depositors who want to fine-tune their risk exposure. Understanding these DeFi risks is worth your time before committing capital.

Yield-bearing stablecoins

Instead of depositing into a lending pool yourself, you can hold a stablecoin that generates yield automatically. Ethena's sUSDe earns from perpetual futures funding rates and staked ETH yield. Sky's sUSDS (formerly sDAI) earns from Sky protocol's lending and real-world asset revenue.

The advantage is simplicity. You hold the token and yield accrues. The risk is that these tokens carry the smart contract risk of the underlying protocol, plus the specific mechanism risk of however that yield is generated. sUSDe, for example, depends on funding rates remaining positive on average. In a prolonged bear market, funding can flip negative for extended periods.

Fixed-rate strategies with Pendle

Pendle lets you split yield-bearing assets into principal and yield components. If you expect rates to fall further, you can lock in today's rate by buying the principal token at a discount. Pendle recently launched a stUSDS pool with Spark Protocol offering around 16.8% APY, though that elevated rate reflects short-term incentives and high borrowing demand rather than sustainable income.

Fixed-rate strategies add complexity. You are dealing with maturity dates (for example, the stUSDS pool matures June 25, 2026), potential liquidity issues if you need to exit early, and the learning curve of understanding yield tokenization. But for someone who wants predictability, locking in 5% to 7% for six months can be more appealing than watching variable rates bounce around.

Stablecoin liquidity provision

Providing liquidity to stablecoin trading pairs (USDC/USDT on Curve, for instance) earns you a share of swap fees. Because stablecoins trade close to $1, impermanent loss is minimal in normal conditions. The risk is a depeg event. If one stablecoin in the pair loses its peg, your position takes a real hit.

In a bear market, trading volumes tend to drop, which means lower fees. This makes LPing less attractive than lending for most people. It still has a role if you are comfortable with the specific pairs and want diversified yield sources.

Tokenized treasuries

The lowest-risk option in DeFi right now is onchain tokenized U.S. Treasury bills. Products from protocols like Ondo, Backed, and Maple give you exposure to short-term government debt with yields around 4% to 5%. The yield comes from the U.S. government, not from crypto markets. The main risks are smart contract risk on the wrapper and potential regulatory changes to the tokenized securities space.

How does the GENIUS Act affect stablecoin yield?

The GENIUS Act, signed into law in 2025, established the first federal regulatory framework for payment stablecoins in the United States. On February 26, 2026, the OCC published a 376-page proposed rulemaking to implement the Act. One of the most talked-about provisions is the yield ban.

Here is what the ban actually says: authorized payment stablecoin issuers (think Circle, Tether, or any bank issuing a regulated stablecoin) are prohibited from distributing yield, interest, or rewards tied to stablecoin ownership. The OCC's draft goes further, creating a "regulatory presumption" that even indirect or affiliate-based reward structures could violate the Act.

But the exemptions matter more than the ban for most DeFi users.

DeFi and self-custody are exempt

The GENIUS Act explicitly excludes distributed ledger protocols (DeFi), development activities, immutable and self-custodial wallet interfaces, and liquidity pool participation from the definition of "digital asset service provider." In plain language: if you are lending USDC on Aave through a self-custody wallet, the yield ban does not apply to you.

This distinction is why the current White House negotiations on stablecoin yield are so important. The administration has held at least three meetings in February 2026 between crypto companies and banks, with the latest on February 19 reportedly making "progress." According to CoinDesk, the White House favors allowing limited stablecoin rewards while banks push back, arguing that yield-bearing stablecoins could compete with their deposit business.

The practical upshot: the yield ban pushes more activity toward DeFi. If Circle cannot pay you yield on USDC directly, your best option is to deposit that USDC into a lending protocol yourself. Self-custody platforms like Pistachio.fi, which use MPC wallets through PortalHQ to keep you in control of your keys, are positioned well for this exact scenario.

Building a bear market stablecoin portfolio

The goal during a bear market is not maximizing yield. It is preserving capital, staying liquid, and earning a real return above inflation while you wait for better conditions. Here is a practical allocation framework.

The core-satellite approach

The core portion (60–70% of holdings) goes into established lending protocols like Aave and Compound, or tokenized treasuries. Accept 3–5% APY in exchange for high liquidity and battle-tested smart contracts. This is your safety net.

The satellite allocation (20–30%) targets higher-yield strategies: Morpho vaults with optimized risk parameters, fixed-rate positions on Pendle, or yield-bearing stablecoins. Target 5–8% APY with slightly higher risk.

Reserve 10–20% as plain stablecoins with no yield exposure. When opportunities appear (a protocol launches new incentives, a temporary dislocation creates elevated rates), you want capital ready to deploy.

Risk management rules that actually matter

Diversify across protocols, not just strategies. If you put everything into Aave, you carry Aave's smart contract risk on 100% of your portfolio.

Check the audit history of any protocol you deposit into. Morpho has 25+ audits. Some newer protocols have one or none.

Watch utilization rates. When a lending pool's utilization climbs above 90%, withdrawal liquidity dries up. You might not be able to exit when you need to.

Avoid chasing double-digit APYs on new protocols. High yields in a bear market almost always come from token emissions that will end, or from mechanisms you do not fully understand. The protocols offering 20%+ on stablecoins right now are either running temporary incentive programs or taking on risk you should know about.

Pistachio.fi addresses several of these concerns structurally. Its curated investment vaults are selected by experts who evaluate protocol risk. Every option carries a risk grade so you can compare before you commit. The platform is completely gasless (zero transaction fees), which means the yield you see is closer to the yield you actually keep. And since Pistachio uses self-custody through MPC wallets, your funds never sit in a custodial hot wallet that could be frozen or hacked.

How does self-custody change the equation?

The 2022 bear market taught a painful lesson. Celsius, Voyager, BlockFi, and FTX all froze withdrawals when conditions deteriorated. Users who had deposited stablecoins for yield found their funds locked in bankruptcy proceedings. Some are still waiting for partial recovery four years later.

Self-custody removes this risk entirely. When you hold your keys (or use an MPC wallet where you control the key shares), no company can prevent you from withdrawing. Your stablecoins sit in smart contracts, not on a company's balance sheet.

This is not just a philosophical preference. It is a regulatory trend. The GENIUS Act's DeFi exemptions effectively reward self-custody users with continued access to yield. The OCC's framework treats custodial stablecoins like stored-value products (no yield allowed), while self-directed DeFi activity remains outside the ban's scope.

Pistachio.fi's approach uses PortalHQ's MPC wallet technology, which splits your private key into shares so that no single party (including Pistachio) can access your funds unilaterally. Combined with its neobank-like interface, it bridges the gap between the security of self-custody and the convenience of a managed platform.

Tax implications of stablecoin yield

Stablecoin yield is taxable income in most jurisdictions, including the United States. The IRS treats DeFi lending interest as ordinary income, taxed at your marginal rate in the year you receive it. This applies whether you claim the yield manually or it auto-compounds.

Tracking this across multiple protocols, chains, and strategies can be a headache. Every deposit, withdrawal, claim, and swap is a taxable event that needs documentation. Pistachio.fi integrates with Awaken.Tax for one-click tax export, which saves hours of spreadsheet work at the end of the year. If you are using multiple protocols manually, make sure you have a tracking solution in place before you start.

Frequently asked questions

What APY can I expect on stablecoins during a bear market?

Most DeFi lending protocols offer 3% to 7% APY on stablecoins during the current bear market. Rates vary based on borrowing demand, with temporary spikes during volatility events. Fixed-rate options through Pendle can lock in 5% to 10%, and yield-bearing stablecoins like sUSDe or sUSDS target 4% to 8%.

Is stablecoin yield still legal under the GENIUS Act?

Yes, for DeFi users. The GENIUS Act's yield ban applies only to custodial payment stablecoin issuers (like Circle or banks). DeFi protocols, self-custody wallets, and liquidity pool participation are explicitly exempt from the ban. The OCC confirmed this in its February 26, 2026 proposed rulemaking.

What is the safest way to earn yield on stablecoins?

The safest approach is lending USDC or USDT on established protocols like Aave or Compound, which have billions in deposits and years of operating history. Tokenized U.S. Treasury products offer even lower risk at 4% to 5% APY, since the yield comes from government bonds rather than crypto borrowing markets. Always use a self-custody wallet to avoid counterparty risk.

Can I lose money on stablecoins?

Yes. Stablecoins can depeg from $1, and the smart contracts holding your deposits can be exploited. Protocol insolvency (as seen with Terra/UST in 2022) can cause total loss. Even well-audited protocols carry residual smart contract risk. Diversifying across protocols and sticking to the most battle-tested options reduces but does not eliminate this risk.

How does Pistachio.fi compare to using DeFi protocols directly?

Pistachio.fi aggregates DeFi yields from vetted protocols into curated vaults, adds expert risk grades, and eliminates gas fees. You maintain self-custody through MPC wallets. The tradeoff compared to direct protocol access is that you rely on Pistachio's curation rather than choosing protocols yourself, and you use their interface rather than interacting with smart contracts directly. For most users, the convenience, risk filtering, and zero gas fees outweigh the reduced control.

Should I move all my crypto to stablecoins during a bear market?

That depends on your conviction and time horizon. Going 100% stablecoins means you avoid further drawdowns, but you also miss the recovery. A common approach is to hold a larger stablecoin allocation than you would during a bull market (say 40% to 60% of your portfolio) and earn yield while you wait. Dollar-cost averaging back into BTC or ETH at lower prices is another option that stablecoin yield can fund.

What happens to stablecoin yields if Bitcoin keeps dropping?

Further price drops typically reduce borrowing demand, which compresses lending yields. However, sharp selloffs can temporarily spike rates as traders scramble to borrow stablecoins for margin calls and liquidations. Over a sustained bear market, expect yields to settle toward the lower end of the 3% to 7% range, but they rarely go to zero because some borrowing demand always exists.

Cross-chain crypto swaps: how Li.Fi powers Pistachio's one-tap zaps (2026)

Etherfuse stablebonds: earn government bond yields on-chain (2026)

How to earn money online in 2026 (crypto yield vs. the rest)

Linea crypto explained: what it is and how it works (2026)

Ethereum wallet guide 2026 (ethernet wallet explained)

DeFi Staking with Stader Labs: How ETHx Works in 2026

High-liquidity crypto exchanges: PancakeSwap guide 2026

What is Raydium? How Solana's AMM Works in 2026

Passive Income Ideas for 2026: 10 Ways That Actually Work

Hong Kong crypto news 2026: licenses, stablecoins, and regulation

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.