Stablecoin Yield: The Complete Guide to Earning Interest on Your Digital Dollars

Stablecoin Yield: The Complete Guide to Earning Interest on Your Digital Dollars

Stablecoin Yield: The Complete Guide to Earning Interest on Your Digital Dollars

Stablecoin Yield: The Complete Guide to Earning Interest on Your Digital Dollars

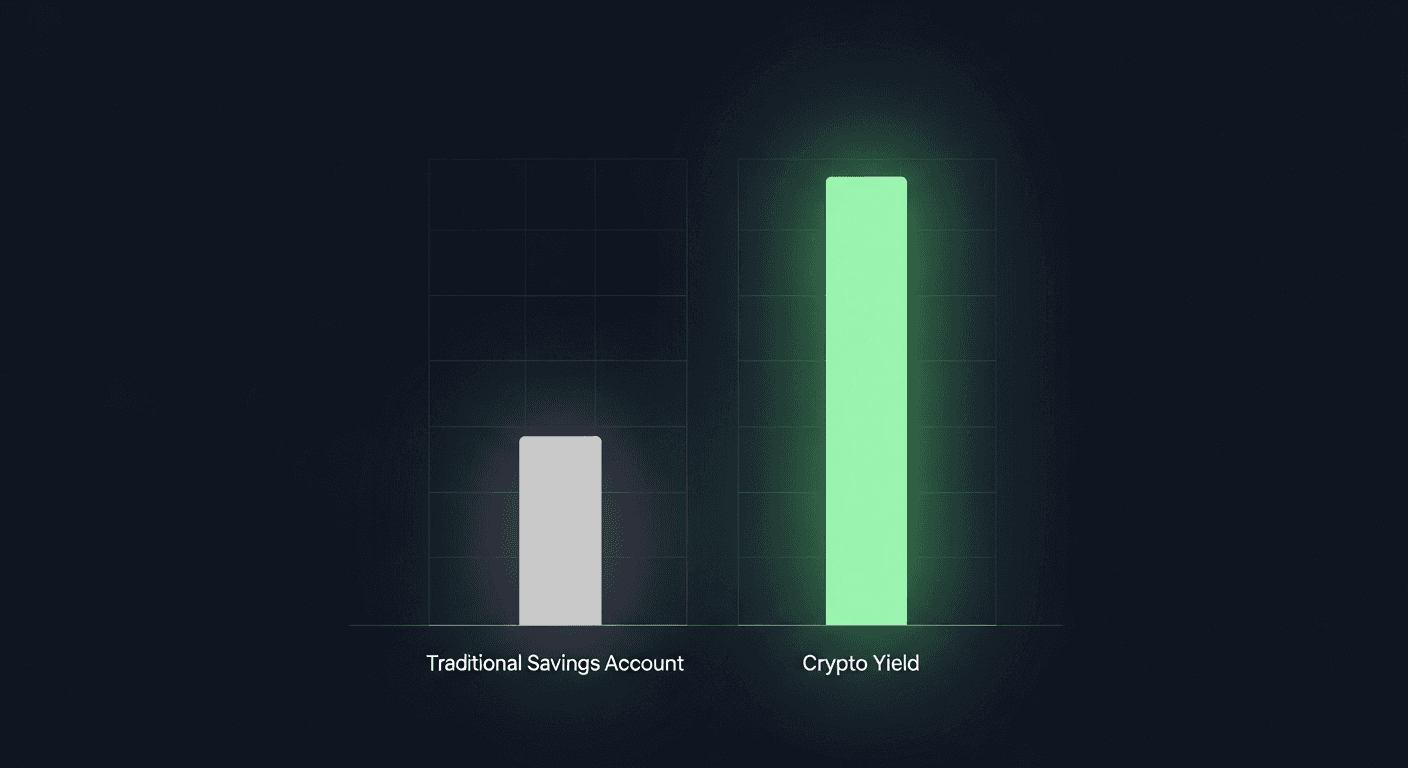

Your savings account probably pays you 0.3% interest. Maybe 0.5% if you're lucky. Meanwhile, stablecoin yields routinely hit 4-8%, with some opportunities reaching double digits. That's not a typo. And it's exactly why traditional banks are spending millions lobbying Congress to shut it down.

Pistachio.fi is a crypto yield platform that helps you access curated stablecoin yield opportunities without navigating DeFi complexity yourself. This guide covers everything you need to know about earning yield on stablecoins in 2026: where the returns come from, what rates you can realistically expect, the regulatory battle happening right now in Washington, and how to get started without getting burned.

Key takeaways

Stablecoin yield comes from lending, liquidity provision, or Treasury-backed reserves, typically returning 4-8% APY.

Current rates: Blue-chip DeFi (Aave) pays 2-7%, CeFi platforms 8-16%, Treasury-backed stablecoins 4-5%.

Regulatory battle: Banks are lobbying to ban yield-bearing stablecoins. The Clarity Act stalled in Congress over this issue.

Risk management: Diversify across protocols, stick with battle-tested platforms, and keep some funds liquid.

What is stablecoin yield?

Stablecoin yield is the return you earn by putting your stablecoins to work instead of letting them sit idle. Stablecoins like USDC and USDT are designed to stay pegged at $1, which means you're not betting on price appreciation. The yield comes from what happens behind the scenes with that capital.

Think of it like a savings account, but one that operates in the decentralized finance ecosystem. You deposit your stablecoins into a protocol or platform. That protocol uses your capital productively. You get paid a share of the returns.

The numbers speak for themselves. The stablecoin market grew 50% in 2025, with total market cap now sitting around $300 billion. A big reason for that growth? Retail investors figured out they could earn 4-5% on crypto platforms while their bank accounts paid them next to nothing. For a broader look at crypto passive income strategies, see our passive income crypto 2026 guide.

Where does stablecoin yield actually come from?

Stablecoin yield comes from three primary sources: lending, liquidity provision, and Treasury-backed reserves. If you don't understand where your yield originates, you can't properly assess the risk.

Lending

The most straightforward source. You deposit stablecoins into a lending protocol. Borrowers pay interest to borrow those stablecoins. You receive a cut of that interest.

On platforms like Aave, this happens automatically through smart contracts. When utilization is low (plenty of supply relative to demand), rates stay modest. When utilization climbs, rates increase to attract more deposits and discourage excessive borrowing.

DeFi lending rates fluctuate constantly based on market conditions. Right now, you can expect anywhere from 2% to 7% on major protocols, with Aave averaging around 6.5% for USDC. Centralized platforms often offer higher rates (8-14%), but they come with different tradeoffs we'll cover later.

Liquidity provision

Decentralized exchanges need liquidity to function. When you swap tokens on Uniswap or Curve, you're trading against liquidity pools funded by other users. Those users earn a share of the trading fees.

For stablecoin pairs (like USDC/USDT), this is relatively low-risk since both assets should stay around $1. You're earning trading fees without the price volatility that makes other liquidity positions risky. Curve Finance pools typically yield between 2% and 19% depending on the specific pool and current trading volume.

The catch? Something called impermanent loss. If the assets in your pool diverge in price, you can end up with less value than if you'd just held the tokens. With stablecoins, this risk is minimal under normal conditions but can spike during market stress or depeg events.

Treasury-backed yield

Here's where things get interesting. Companies like Circle (USDC issuer) hold reserves to back their stablecoins. Those reserves sit in bank accounts and short-term Treasury bills. Treasury bills currently yield around 4-5%.

Traditional stablecoins like USDC don't pass this yield to holders. Circle keeps it. But a new category of yield-bearing stablecoins does share this Treasury income with users. Products like Mountain Protocol's USDM and BlackRock's BUIDL fund invest reserves in T-bills and distribute the interest to token holders.

This is also the mechanism that has banks terrified. More on that shortly.

What are the current stablecoin interest rates?

Rates change constantly, but here's a realistic snapshot of what the market looks like in January 2026.

Platform Type | Typical USDC/USDT Yield | Notes |

|---|---|---|

Blue-chip DeFi (Aave, Compound) | 2% - 7% | Variable rates, no lockups, transparent |

Optimized DeFi (Morpho, Yearn) | 3% - 12% | Higher yields through strategy optimization |

CeFi Platforms (Nexo, Ledn) | 8% - 16% | Higher rates often require token holdings or lockups |

Treasury-backed (USDM, BUIDL) | 4% - 5% | Backed by T-bills, daily distribution |

Liquidity Pools (Curve) | 2% - 19% | Varies by pool volume and incentives |

A word of caution: anything promising 20%+ on stablecoins should raise immediate red flags. Those rates typically involve either significant hidden risks, unsustainable token incentives, or outright fraud. The 2022 crypto lending implosions taught everyone this lesson the hard way.

Why are banks trying to ban stablecoin yields?

If you've been following crypto news, you've probably seen headlines about the Digital Asset Market Clarity Act grinding to a halt in Congress. The story behind that stall reveals something important about the future of stablecoin yields.

The Clarity Act was supposed to be the comprehensive framework that finally gave crypto markets regulatory clarity in the US. It passed the House and seemed headed for Senate approval. Then everything fell apart over a single issue: whether stablecoin issuers can share yield with their users.

What banks are arguing

Banking lobby groups have characterized yield-bearing stablecoins as an "extinction-level event" for their members. That's not hyperbole. That's their actual language in lobbying documents.

Their argument: if stablecoin issuers can pass Treasury bill yields to users, deposits will flood out of traditional banks and into stablecoins. Why keep money in a savings account earning 0.3% when a stablecoin pays 4%? For more on how crypto yields compare to traditional options, see our crypto vs Treasury yield comparison.

America's Credit Unions has explicitly called for a "ban on stablecoin inducements" in any final legislation. The banking industry wants to make it illegal for stablecoin issuers to offer any compensation to holders, whether that's advertised yields, promotional rewards, or interest-like payments.

The crypto industry's response

Coinbase CEO Brian Armstrong hasn't been shy about calling this what it is. In a recent FOX Business interview, he said banks were using "regulatory capture to ban competition" and that the restrictions "just felt deeply unfair."

The data backs him up. Research from Charles River Associates found no statistically significant relationship between USDC growth and community-bank deposits. People using stablecoins aren't treating them as bank account substitutes. They're different products serving different needs.

Coinbase's chief policy officer Faryar Shirzad has also pointed out the global implications. China's digital yuan became interest-bearing as of January 1, 2026. If the US bans yield-bearing dollar stablecoins while competitors offer interest, it undermines dollar dominance in digital payments.

Where things stand now

The Senate Banking Committee postponed its vote on the Clarity Act on January 15, 2026. The White House is reportedly considering withdrawing support entirely. The standoff centers on stablecoin yield provisions worth roughly $1 billion in annual revenue for Coinbase alone.

This isn't just a policy debate. It's a fight over whether traditional finance can use regulation to protect itself from competition. The outcome will shape what yields are legally available to US users for years to come.

For now, existing yield opportunities remain available. But anyone earning stablecoin yield should understand this regulatory uncertainty is part of the picture.

What are the risks of stablecoin yield?

Stablecoin yields aren't free money. Every percentage point of return comes with corresponding risks. Here's what can actually go wrong.

Smart contract risk

When you deposit into a DeFi protocol, your funds are controlled by code. If that code has a bug, a vulnerability, or gets exploited, your funds can disappear. No insurance. No recourse. Recovery is never guaranteed. For tips on protecting yourself, read how to stop getting hacked.

This risk is why protocol selection matters. Battle-tested protocols like Aave (with over $10 billion in total value locked) have survived years of attacks and scrutiny. New protocols offering suspiciously high yields haven't proven themselves.

Depeg risk

Stablecoins are designed to stay at $1, but they don't always succeed. USDC briefly depegged during the Silicon Valley Bank crisis in 2023. More dramatic examples like UST's collapse wiped out billions.

Even temporary deviations can hurt you if you need to exit a position, rebalance, or repay a loan during the depeg. The safest stablecoins (USDC, USDT) have the strongest track records, but no peg is guaranteed.

Counterparty risk

If you're using a centralized platform, you're trusting that company to remain solvent, honest, and operational. The 2022 wave of CeFi bankruptcies (Celsius, BlockFi, Voyager) showed how quickly that trust can be misplaced.

DeFi reduces counterparty risk by removing the middleman, but introduces smart contract risk instead. There's no free lunch.

Liquidity risk

Can you actually withdraw when you need to? During market stress, platforms can pause withdrawals. Protocols can implement emergency stops. Liquidity pools can dry up. That 8% yield means nothing if you can't access your funds when you need them.

Regulatory risk

As the Clarity Act battle shows, the rules can change. Platforms can lose licenses. Products can be restricted by geography. Yields that are legal today might not be tomorrow.

How do you earn stablecoin yield safely?

Risk management isn't about avoiding all risk. It's about taking calculated risks you understand and can afford. Here's the framework.

Start small and diversify

Don't put all your stablecoins in one protocol or platform. Spread across multiple venues. If one fails, you've lost a portion, not everything.

Prioritize established protocols

The highest yields are often the most dangerous. Stick with protocols that have been operating for years, have significant total value locked, and have survived multiple market cycles without incident.

Understand what you're buying

If you can't explain in plain language where your yield comes from, you probably shouldn't be earning it. Complexity is where risks hide.

Keep some funds liquid

Don't lock up everything chasing an extra 2%. Having stablecoins you can access immediately gives you options during market stress.

Use tools that help you evaluate risk

This is where most people get stuck. Evaluating DeFi protocols requires understanding smart contract audits, team backgrounds, tokenomics, and historical performance. Most people don't have time to become experts in protocol analysis.

Getting started with Pistachio.fi

We built Pistachio.fi specifically because stablecoin yield shouldn't require a PhD in smart contract security.

Our Curated Investment Vaults do the protocol research for you. We analyze the ecosystem, evaluate the risks, and select opportunities that meet our standards. You're not picking blindly from hundreds of options. You're choosing from a shortlist we've already vetted.

Every option comes with an Expert Risk Grade. We rate protocols based on smart contract security, team credibility, historical performance, and liquidity conditions. You can see exactly what you're getting into before you commit a single dollar.

The experience is completely gasless. No transaction fees eating into your returns. No calculating whether the yield is even worth it after gas costs. We handle that infrastructure so you don't have to think about it. Learn more about how smart accounts enable gasless transactions.

And when tax season comes, you can export your entire Pistachio portfolio directly to Awaken.Tax with one click. No spreadsheets. No manual transaction hunting. Your positions, gains, and cost basis flow straight into professional tax software.

Stablecoin yield is real. The opportunities are legitimate. But the difference between earning sustainable returns and losing your principal often comes down to the tools you use and the decisions you make.

What it comes down to

Stablecoin yield is one of the clearer advantages crypto offers over traditional finance. You can earn 4-8% on dollar-denominated assets while your bank pays you a fraction of a percent. That's not a temporary arbitrage. It's a structural difference in how these systems operate.

But the regulatory battle happening right now in Washington will determine whether these opportunities remain available to US users. Banks want to make yield-bearing stablecoins illegal. Crypto advocates are fighting to keep them accessible. The outcome isn't certain.

What is certain: if you're going to earn stablecoin yield, you need to understand where it comes from, what risks you're taking, and how to manage those risks. Chase the highest number without understanding the mechanics and you'll eventually learn why those rates were so high.

Start with protocols you trust. Spread your exposure across multiple venues. Keep some funds you can access immediately. Use tools that help you evaluate risk rather than obscure it. The yields are real. The risks are manageable. You just have to approach it the right way.

Last updated: January 2026

Frequently asked questions

Is stablecoin yield safe?

Stablecoin yield carries risks including smart contract vulnerabilities, stablecoin depeg events, and platform failures. Blue-chip DeFi protocols like Aave have strong track records, but no yield is risk-free. Diversifying across multiple protocols helps manage these risks.

How much can I earn on stablecoin yield?

Current rates range from 2-7% on major DeFi protocols (Aave, Compound), 4-5% on Treasury-backed stablecoins (USDM, BUIDL), and 8-16% on CeFi platforms. Anything promising 20%+ should be viewed with extreme skepticism.

What's the difference between DeFi and CeFi stablecoin yield?

DeFi yield comes from on-chain protocols controlled by smart contracts. You keep custody of your assets but face smart contract risk. CeFi yield comes from centralized companies. They manage your funds, which introduces counterparty risk if the company fails.

Can stablecoins lose their peg?

Yes. USDC briefly fell to $0.86 during the Silicon Valley Bank crisis in 2023. UST's collapse in 2022 was more dramatic. Major stablecoins like USDC and USDT have recovered from temporary depegs, but the risk exists.

Are stablecoin yields taxable?

In the US, stablecoin yield is generally treated as ordinary income and taxed at your regular income tax rate. You should report earnings when received. Consult a tax professional for your specific situation.

Your savings account probably pays you 0.3% interest. Maybe 0.5% if you're lucky. Meanwhile, stablecoin yields routinely hit 4-8%, with some opportunities reaching double digits. That's not a typo. And it's exactly why traditional banks are spending millions lobbying Congress to shut it down.

Pistachio.fi is a crypto yield platform that helps you access curated stablecoin yield opportunities without navigating DeFi complexity yourself. This guide covers everything you need to know about earning yield on stablecoins in 2026: where the returns come from, what rates you can realistically expect, the regulatory battle happening right now in Washington, and how to get started without getting burned.

Key takeaways

Stablecoin yield comes from lending, liquidity provision, or Treasury-backed reserves, typically returning 4-8% APY.

Current rates: Blue-chip DeFi (Aave) pays 2-7%, CeFi platforms 8-16%, Treasury-backed stablecoins 4-5%.

Regulatory battle: Banks are lobbying to ban yield-bearing stablecoins. The Clarity Act stalled in Congress over this issue.

Risk management: Diversify across protocols, stick with battle-tested platforms, and keep some funds liquid.

What is stablecoin yield?

Stablecoin yield is the return you earn by putting your stablecoins to work instead of letting them sit idle. Stablecoins like USDC and USDT are designed to stay pegged at $1, which means you're not betting on price appreciation. The yield comes from what happens behind the scenes with that capital.

Think of it like a savings account, but one that operates in the decentralized finance ecosystem. You deposit your stablecoins into a protocol or platform. That protocol uses your capital productively. You get paid a share of the returns.

The numbers speak for themselves. The stablecoin market grew 50% in 2025, with total market cap now sitting around $300 billion. A big reason for that growth? Retail investors figured out they could earn 4-5% on crypto platforms while their bank accounts paid them next to nothing. For a broader look at crypto passive income strategies, see our passive income crypto 2026 guide.

Where does stablecoin yield actually come from?

Stablecoin yield comes from three primary sources: lending, liquidity provision, and Treasury-backed reserves. If you don't understand where your yield originates, you can't properly assess the risk.

Lending

The most straightforward source. You deposit stablecoins into a lending protocol. Borrowers pay interest to borrow those stablecoins. You receive a cut of that interest.

On platforms like Aave, this happens automatically through smart contracts. When utilization is low (plenty of supply relative to demand), rates stay modest. When utilization climbs, rates increase to attract more deposits and discourage excessive borrowing.

DeFi lending rates fluctuate constantly based on market conditions. Right now, you can expect anywhere from 2% to 7% on major protocols, with Aave averaging around 6.5% for USDC. Centralized platforms often offer higher rates (8-14%), but they come with different tradeoffs we'll cover later.

Liquidity provision

Decentralized exchanges need liquidity to function. When you swap tokens on Uniswap or Curve, you're trading against liquidity pools funded by other users. Those users earn a share of the trading fees.

For stablecoin pairs (like USDC/USDT), this is relatively low-risk since both assets should stay around $1. You're earning trading fees without the price volatility that makes other liquidity positions risky. Curve Finance pools typically yield between 2% and 19% depending on the specific pool and current trading volume.

The catch? Something called impermanent loss. If the assets in your pool diverge in price, you can end up with less value than if you'd just held the tokens. With stablecoins, this risk is minimal under normal conditions but can spike during market stress or depeg events.

Treasury-backed yield

Here's where things get interesting. Companies like Circle (USDC issuer) hold reserves to back their stablecoins. Those reserves sit in bank accounts and short-term Treasury bills. Treasury bills currently yield around 4-5%.

Traditional stablecoins like USDC don't pass this yield to holders. Circle keeps it. But a new category of yield-bearing stablecoins does share this Treasury income with users. Products like Mountain Protocol's USDM and BlackRock's BUIDL fund invest reserves in T-bills and distribute the interest to token holders.

This is also the mechanism that has banks terrified. More on that shortly.

What are the current stablecoin interest rates?

Rates change constantly, but here's a realistic snapshot of what the market looks like in January 2026.

Platform Type | Typical USDC/USDT Yield | Notes |

|---|---|---|

Blue-chip DeFi (Aave, Compound) | 2% - 7% | Variable rates, no lockups, transparent |

Optimized DeFi (Morpho, Yearn) | 3% - 12% | Higher yields through strategy optimization |

CeFi Platforms (Nexo, Ledn) | 8% - 16% | Higher rates often require token holdings or lockups |

Treasury-backed (USDM, BUIDL) | 4% - 5% | Backed by T-bills, daily distribution |

Liquidity Pools (Curve) | 2% - 19% | Varies by pool volume and incentives |

A word of caution: anything promising 20%+ on stablecoins should raise immediate red flags. Those rates typically involve either significant hidden risks, unsustainable token incentives, or outright fraud. The 2022 crypto lending implosions taught everyone this lesson the hard way.

Why are banks trying to ban stablecoin yields?

If you've been following crypto news, you've probably seen headlines about the Digital Asset Market Clarity Act grinding to a halt in Congress. The story behind that stall reveals something important about the future of stablecoin yields.

The Clarity Act was supposed to be the comprehensive framework that finally gave crypto markets regulatory clarity in the US. It passed the House and seemed headed for Senate approval. Then everything fell apart over a single issue: whether stablecoin issuers can share yield with their users.

What banks are arguing

Banking lobby groups have characterized yield-bearing stablecoins as an "extinction-level event" for their members. That's not hyperbole. That's their actual language in lobbying documents.

Their argument: if stablecoin issuers can pass Treasury bill yields to users, deposits will flood out of traditional banks and into stablecoins. Why keep money in a savings account earning 0.3% when a stablecoin pays 4%? For more on how crypto yields compare to traditional options, see our crypto vs Treasury yield comparison.

America's Credit Unions has explicitly called for a "ban on stablecoin inducements" in any final legislation. The banking industry wants to make it illegal for stablecoin issuers to offer any compensation to holders, whether that's advertised yields, promotional rewards, or interest-like payments.

The crypto industry's response

Coinbase CEO Brian Armstrong hasn't been shy about calling this what it is. In a recent FOX Business interview, he said banks were using "regulatory capture to ban competition" and that the restrictions "just felt deeply unfair."

The data backs him up. Research from Charles River Associates found no statistically significant relationship between USDC growth and community-bank deposits. People using stablecoins aren't treating them as bank account substitutes. They're different products serving different needs.

Coinbase's chief policy officer Faryar Shirzad has also pointed out the global implications. China's digital yuan became interest-bearing as of January 1, 2026. If the US bans yield-bearing dollar stablecoins while competitors offer interest, it undermines dollar dominance in digital payments.

Where things stand now

The Senate Banking Committee postponed its vote on the Clarity Act on January 15, 2026. The White House is reportedly considering withdrawing support entirely. The standoff centers on stablecoin yield provisions worth roughly $1 billion in annual revenue for Coinbase alone.

This isn't just a policy debate. It's a fight over whether traditional finance can use regulation to protect itself from competition. The outcome will shape what yields are legally available to US users for years to come.

For now, existing yield opportunities remain available. But anyone earning stablecoin yield should understand this regulatory uncertainty is part of the picture.

What are the risks of stablecoin yield?

Stablecoin yields aren't free money. Every percentage point of return comes with corresponding risks. Here's what can actually go wrong.

Smart contract risk

When you deposit into a DeFi protocol, your funds are controlled by code. If that code has a bug, a vulnerability, or gets exploited, your funds can disappear. No insurance. No recourse. Recovery is never guaranteed. For tips on protecting yourself, read how to stop getting hacked.

This risk is why protocol selection matters. Battle-tested protocols like Aave (with over $10 billion in total value locked) have survived years of attacks and scrutiny. New protocols offering suspiciously high yields haven't proven themselves.

Depeg risk

Stablecoins are designed to stay at $1, but they don't always succeed. USDC briefly depegged during the Silicon Valley Bank crisis in 2023. More dramatic examples like UST's collapse wiped out billions.

Even temporary deviations can hurt you if you need to exit a position, rebalance, or repay a loan during the depeg. The safest stablecoins (USDC, USDT) have the strongest track records, but no peg is guaranteed.

Counterparty risk

If you're using a centralized platform, you're trusting that company to remain solvent, honest, and operational. The 2022 wave of CeFi bankruptcies (Celsius, BlockFi, Voyager) showed how quickly that trust can be misplaced.

DeFi reduces counterparty risk by removing the middleman, but introduces smart contract risk instead. There's no free lunch.

Liquidity risk

Can you actually withdraw when you need to? During market stress, platforms can pause withdrawals. Protocols can implement emergency stops. Liquidity pools can dry up. That 8% yield means nothing if you can't access your funds when you need them.

Regulatory risk

As the Clarity Act battle shows, the rules can change. Platforms can lose licenses. Products can be restricted by geography. Yields that are legal today might not be tomorrow.

How do you earn stablecoin yield safely?

Risk management isn't about avoiding all risk. It's about taking calculated risks you understand and can afford. Here's the framework.

Start small and diversify

Don't put all your stablecoins in one protocol or platform. Spread across multiple venues. If one fails, you've lost a portion, not everything.

Prioritize established protocols

The highest yields are often the most dangerous. Stick with protocols that have been operating for years, have significant total value locked, and have survived multiple market cycles without incident.

Understand what you're buying

If you can't explain in plain language where your yield comes from, you probably shouldn't be earning it. Complexity is where risks hide.

Keep some funds liquid

Don't lock up everything chasing an extra 2%. Having stablecoins you can access immediately gives you options during market stress.

Use tools that help you evaluate risk

This is where most people get stuck. Evaluating DeFi protocols requires understanding smart contract audits, team backgrounds, tokenomics, and historical performance. Most people don't have time to become experts in protocol analysis.

Getting started with Pistachio.fi

We built Pistachio.fi specifically because stablecoin yield shouldn't require a PhD in smart contract security.

Our Curated Investment Vaults do the protocol research for you. We analyze the ecosystem, evaluate the risks, and select opportunities that meet our standards. You're not picking blindly from hundreds of options. You're choosing from a shortlist we've already vetted.

Every option comes with an Expert Risk Grade. We rate protocols based on smart contract security, team credibility, historical performance, and liquidity conditions. You can see exactly what you're getting into before you commit a single dollar.

The experience is completely gasless. No transaction fees eating into your returns. No calculating whether the yield is even worth it after gas costs. We handle that infrastructure so you don't have to think about it. Learn more about how smart accounts enable gasless transactions.

And when tax season comes, you can export your entire Pistachio portfolio directly to Awaken.Tax with one click. No spreadsheets. No manual transaction hunting. Your positions, gains, and cost basis flow straight into professional tax software.

Stablecoin yield is real. The opportunities are legitimate. But the difference between earning sustainable returns and losing your principal often comes down to the tools you use and the decisions you make.

What it comes down to

Stablecoin yield is one of the clearer advantages crypto offers over traditional finance. You can earn 4-8% on dollar-denominated assets while your bank pays you a fraction of a percent. That's not a temporary arbitrage. It's a structural difference in how these systems operate.

But the regulatory battle happening right now in Washington will determine whether these opportunities remain available to US users. Banks want to make yield-bearing stablecoins illegal. Crypto advocates are fighting to keep them accessible. The outcome isn't certain.

What is certain: if you're going to earn stablecoin yield, you need to understand where it comes from, what risks you're taking, and how to manage those risks. Chase the highest number without understanding the mechanics and you'll eventually learn why those rates were so high.

Start with protocols you trust. Spread your exposure across multiple venues. Keep some funds you can access immediately. Use tools that help you evaluate risk rather than obscure it. The yields are real. The risks are manageable. You just have to approach it the right way.

Last updated: January 2026

Frequently asked questions

Is stablecoin yield safe?

Stablecoin yield carries risks including smart contract vulnerabilities, stablecoin depeg events, and platform failures. Blue-chip DeFi protocols like Aave have strong track records, but no yield is risk-free. Diversifying across multiple protocols helps manage these risks.

How much can I earn on stablecoin yield?

Current rates range from 2-7% on major DeFi protocols (Aave, Compound), 4-5% on Treasury-backed stablecoins (USDM, BUIDL), and 8-16% on CeFi platforms. Anything promising 20%+ should be viewed with extreme skepticism.

What's the difference between DeFi and CeFi stablecoin yield?

DeFi yield comes from on-chain protocols controlled by smart contracts. You keep custody of your assets but face smart contract risk. CeFi yield comes from centralized companies. They manage your funds, which introduces counterparty risk if the company fails.

Can stablecoins lose their peg?

Yes. USDC briefly fell to $0.86 during the Silicon Valley Bank crisis in 2023. UST's collapse in 2022 was more dramatic. Major stablecoins like USDC and USDT have recovered from temporary depegs, but the risk exists.

Are stablecoin yields taxable?

In the US, stablecoin yield is generally treated as ordinary income and taxed at your regular income tax rate. You should report earnings when received. Consult a tax professional for your specific situation.

Cross-chain crypto swaps: how Li.Fi powers Pistachio's one-tap zaps (2026)

Etherfuse stablebonds: earn government bond yields on-chain (2026)

How to earn money online in 2026 (crypto yield vs. the rest)

Linea crypto explained: what it is and how it works (2026)

Ethereum wallet guide 2026 (ethernet wallet explained)

DeFi Staking with Stader Labs: How ETHx Works in 2026

High-liquidity crypto exchanges: PancakeSwap guide 2026

What is Raydium? How Solana's AMM Works in 2026

Passive Income Ideas for 2026: 10 Ways That Actually Work

Hong Kong crypto news 2026: licenses, stablecoins, and regulation

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.

©2026 Copyright, PistachioFi Inc.